WW NAND Semiconductor Market Revenue Grew Only 4% in 2015 – Gartner

Fueled by elevated supply bit growth that resulted in agressive pricing environment

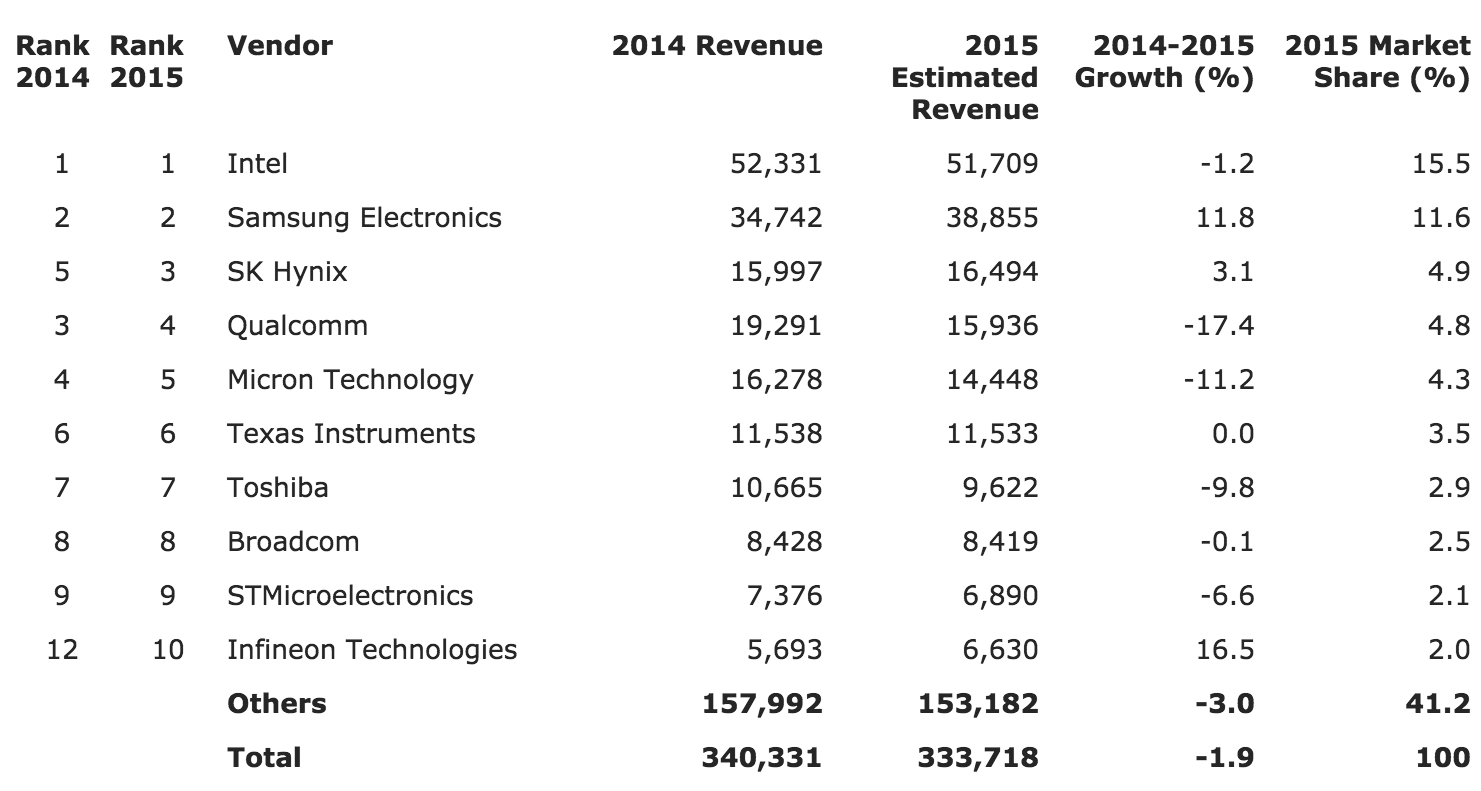

This is a Press Release edited by StorageNewsletter.com on January 12, 2016 at 2:52 pmWorldwide semiconductor revenue totaled $333.7 billion in 2015, a 1.9% decrease from 2014 revenue of $340.3 billion, according to preliminary results by Gartner, Inc.‘s report Market Share Analysis: Semiconductors, Worldwide, Preliminary 2015 Estimates (17 pages, $1,295).

The top 25 semiconductor vendors’ combined revenue increased 0.2%, which was more than the overall industry’s growth. The top 25 vendors accounted for 73.2% of total market revenue, up from 71.7% in 2014.

“Weakened demand for key electronic equipment, the continuing impact of the strong dollar in some regions and elevated inventory are to blame for the decline in the market in 2015,” said Sergis Mushell, research director, Gartner. “In contrast to 2014, which saw revenue growth in all key device categories, 2015 saw mixed performance with optoelectronics, nonoptical sensors, analog and ASIC all reporting revenue growth while the rest of the market saw declines. Strongest growth was from the ASIC segment with growth of 2.4% due to demand from Apple, followed by analog and nonoptical sensors with 1.9% and 1.6% growth, respectively. Memory, the most volatile segment of the semiconductor industry, saw revenue decline by 0.6%, with DRAM experiencing negative growth and NAND flash experiencing growth.”

Intel recorded a 1.2% revenue decline, due to falls in PC shipments. However, it retained the number one market share position for the 24th year in a row with 15.5% market share. Samsung’s memory business helped drive growth of 11.8% in 2015, and the company maintained the number two spot with 11.6% market share.

Top 10 Semiconductor Vendors by Revenue, Worldwide, 2015

(in $ million)

(Source: Gartner, January 2016)

“The rise of the U.S. dollar against a number of different currencies impacted the total semiconductor market in 2015,” said Mushell. “End equipment demand was weakened in regions where the local currency depreciated against the dollar. For example in the eurozone, the sales prices of mobile phones or PCs increased in local currency, as many of the components are priced in U.S. dollars. This resulted in buyers either delaying purchases or buying cheaper substitute products, resulting in lower semiconductor sales. Additionally, Gartner’s semiconductor revenue statistics are based on U.S. dollars; thus, sharp depreciation of the Japanese yen shrinks the revenue and the market share of the Japanese semiconductor vendors when measured in U.S. dollars.”

The NAND market continued to deteriorate throughout the year. As a result, revenue grew only 4.1% in 2015, fueled by elevated supply bit growth that resulted in an aggressive pricing environment. The tumultuous NAND pricing environment rippled through most of the NAND solutions, particularly SSDs, which continue to encroach on HDDs. The ensuing price war in SSDs further pressured the profitability of the NAND flash makers amid the biggest technology transition in flash history – 3D NAND. While 3D NAND commercialization was modest, it was limited to only one vendor – Samsung. Modest revenue gains have not stopped investment in NAND flash and 3D technology, with all vendors continuing to spend aggressively in the technology and most with new fabs.

After 32.0% revenue growth in 2014, the DRAM market hit a downturn in 2015. An oversupply in the commodity portion of the market caused by weak PC demand led to severe declines in ASPs, and revenue contracted by 2.4% compared with 2014. The oversupply and the extent of ASP declines could have been worse if Micron Technologies’ bit growth had performed in line with its South Korean rivals. Fortunately for the market, the company saw negative bit growth due to its transition to 20nm, sparing the industry from an even more severe downturn.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter